SoFiUSD: The Stablecoin Leading Banks into the Blockchain

By: WEEX|2026/05/28 19:30:00

0

Share

In 2026, stablecoins finally moved beyond crypto exchanges to become part of the banking infrastructure narrative. While the digital dollar was previously associated primarily with USDT, USDC, or the DeFi market, regulated financial institutions are now entering the game more actively. One of the most notable examples is SoFiUSD, a stablecoin from SoFi Bank.

This topic is important not only for traders. Bank stablecoins can impact international payments, B2B settlements, the tokenization of deposits, fintech products, and regulatory compliance.

SoFiUSD is a digital asset pegged to the US dollar and issued by a banking entity. Its concept is simple: combine the speed of the blockchain with a reserve model that is more familiar to TradFi. However, this does not mean that such a tool is automatically safe or suitable for everyone.

What is SoFiUSD

SoFiUSD, or SOFID, is a payment stablecoin issued by the American national bank SoFi Bank, N.A., which is regulated by the Office of the Comptroller of the Currency (OCC). In May 2026, SoFi announced that SoFiUSD had become available to users of the SoFi app for buying, selling, holding, and converting.

In practice, SoFiUSD functions as a digital dollar: its value is intended to be maintained close to 1 USD, and its reserves are expected to consist primarily of cash or cash equivalents. This distinguishes it from volatile cryptocurrencies like Bitcoin or Ethereum, whose prices are market-driven without a fiat peg.

At the same time, SoFiUSD is not a bank deposit. It is not insured by the Federal Deposit Insurance Corporation (FDIC) or the Securities Investor Protection Corporation (SIPC), is not legal tender, and may lose value. This is a key clarification: the word "bank" in the category name does not equal a guarantee of risk-free status.

Why banks are issuing stablecoins

Banks are interested in stablecoins not because they want to copy crypto exchanges. They are attracted by the infrastructure aspect: 24/7 settlements, faster international transfers, programmable payments, and the potential tokenization of traditional financial products.

In the classic system, a payment may pass through several correspondent banks, payment networks, and time zones. The blockchain does not remove all legal processes and compliance issues, but it can change the technical layer of value transfer. This is precisely why Mastercard, Visa, PayPal, banks, and fintech companies are testing or launching products related to stablecoins.

How SoFiUSD works

SoFiUSD is designed as a dollar-backed stablecoin. The idea is that every token must correspond to dollar value in reserves, and users can convert it back to USD according to the issuer's rules.

At the time of launch, SoFiUSD supported Ethereum and Solana. This is important because the network determines speed, transaction costs, compatibility with crypto wallets, and potential use cases. Ethereum has a broad infrastructure for DeFi and tokenized assets, while Solana is often used for fast and cheaper transactions.

The principle of digital dollar backing

The backing of SoFiUSD must be based on reserves in cash or cash equivalents. This model is closer to USDC or PYUSD than to algorithmic stablecoins, which maintain their peg through market mechanisms and other tokens.

For the user, this means three things:

- it is necessary to look not only at the 1:1 peg statement but also at the quality of the reserves;

- regular attestations or audit confirmations are important;

- liquidity depends on the issuer's rules, available networks, and market infrastructure.

Even a fully backed stablecoin does not eliminate all risks. Technical glitches, delays, address blocking, regulatory restrictions, or loss of wallet access are possible.

The role of blockchain infrastructure

In the case of SoFiUSD, the blockchain acts as a payment and settlement layer. It allows for the transfer of tokens between addresses, the verification of transactions on the network, and the integration of the asset into digital financial services.

Its advantage is not magic, but technical standardization. The token can operate within the infrastructure of wallets, exchanges, payment services, and smart contracts. However, this same openness creates risks: erroneous transfers are often irreversible, and interaction with smart contracts requires extra caution.

Banks and cryptocurrencies in 2026

In 2026, banks can no longer ignore digital assets. They do not necessarily adopt the crypto-ideology of decentralization, but they are actively exploring the blockchain as infrastructure for settlements, custodial services, and tokenization.

SoFiUSD shows one of the possible paths: the bank does not just give clients the ability to buy cryptocurrency, but issues its own digital dollar instrument. This creates a hybrid model between traditional banking and Web3.

In such a model, the user gets the familiar interface of a banking app, but operations can pass through a public blockchain network. For the mass market, this is important: most people do not want to deal with the technical details of private keys, networks, and gas fees before they understand the basic utility of the product.

How banks use blockchain

Banks use blockchain not only for stablecoins. Among the main directions are tokenized deposits, digital bonds, on-chain settlements, compliance automation, and interbank payments.

Integrating blockchain into traditional finance

In traditional finance, many processes still depend on batch processing, working hours, and intermediaries. Blockchain can make some settlements faster, but it does not cancel regulatory requirements. Banks must verify clients, control money laundering risks, comply with sanctions lists, and fulfill the requirements of regulatory bodies.

This is where bank stablecoins differ from most crypto-native assets. They may be less open in terms of access, but more understandable to regulatory bodies and corporate clients.

Digital banking and crypto-banking

Crypto-banking is not banking without rules. It is rather a financial service where a user can work with fiat currencies, digital assets, tokenized products, and blockchain payments in one environment.

The advantage of such a model is convenience. The risk is the concentration of control in one provider. If a user holds assets inside a banking app, they depend on the platform's rules, jurisdiction, requirements, and technical availability of the service.

SoFiUSD and international payments

International transfers remain one of the strongest reasons for interest in stablecoins. A classic bank transfer can be slow and expensive, and fees can be hidden. Stablecoins offer a different approach: a digital dollar can be transferred on the blockchain without being tied to banking hours.

In partnership with Mastercard, SoFi plans to use SoFiUSD as one of the settlement options in the global payment network. This does not mean an immediate replacement of SWIFT or bank transfers. But it shows that stablecoins are becoming not just a crypto-exchange tool, but also part of the payment infrastructure.

Cross-border transfers

For cross-border transfers, stablecoins can be useful where speed, predictable cost, and uninterrupted availability are important. This applies to freelancers, small businesses, international contractors, and companies working with multiple jurisdictions.

But in real life, a transfer is not just a technical transaction. One must consider KYC, anti-money laundering (AML) measures, tax consequences, sanctions restrictions, platform limits, and rules for withdrawal into fiat currencies.

B2B payments in stablecoins

B2B payments are one of the most practical scenarios for bank stablecoins. Companies can use them for settlements with contractors, trading partners, or payment service providers.

The advantage for business is the speed and predictability of the dollar unit of account. The disadvantage is the need for clear bookkeeping, tax accounting, and legal support. For Ukrainian companies, this is especially important, as local legislation regarding virtual assets is still developing.

Blockchain payments and new payment systems

Blockchain payments are often compared to traditional banking systems. Such a comparison is useful, but it should not be simplified. Blockchain can transfer a token faster, but it does not always solve problems related to compliance, refunds, or legal disputes faster.

Therefore, blockchain payments should not be perceived as a universally better replacement. It is a different set of trade-offs.

Stablecoin regulation and financial requirements

Stablecoins have become too large a segment to remain outside the attention of regulatory bodies. According to the Ukrainian financial media Minfin, in 2026, stablecoins are already playing the role of the base layer of the crypto-economy, and they are used not only for trading but also for transfers, store of value, and digital settlements.

Regulatory bodies look at stablecoins through several questions: who is the issuer, what reserves support the token, is there a right to redemption, who controls compliance, how do sanctions restrictions work, and what happens in the event of a liquidity crisis.

KYC and AML

KYC means client verification, and AML means anti-money laundering measures. For bank stablecoins, this is not an optional feature, but a basic part of the model.

Users can expect that access to SoFiUSD will depend on identification rules, jurisdiction, sanctions status, and internal platform rules. This makes the product closer to the banking environment, but less open compared to decentralized crypto-assets.

MiCA and crypto-regulation

In the EU, the MiCA regulation sets rules for issuers of crypto-assets, including stablecoins. Ukrainian media have already noted that MiCA could change the availability of certain stablecoins in the European Economic Area and increase requirements for issuers.

For SoFiUSD, this has indirect significance. The token is issued by an American bank, but the global availability of digital assets depends not only on the issuer's country. If the product or related services enter EU markets, they will have to take local rules into account.

What SoFiUSD means for Ukrainian users

Ukrainian users should view SoFiUSD not as a "new dollar for payments," but as a foreign digital asset with its own access rules. In Ukraine, the hryvnia remains the only legal tender, and full-scale regulation of virtual assets is still in the process of being finalized.

Practical conclusions for Ukraine:

- stablecoins do not replace the hryvnia as legal tender;

- operations with digital assets may have tax consequences;

- access to SoFiUSD may depend on the user's jurisdiction and SoFi's rules;

- sanctions requirements and AML requirements may affect transfers and the blocking of operations;

- businesses need a separate accounting and legal analysis before using stablecoins in settlements.

This does not make SoFiUSD a bad or good tool. It means that it must be evaluated in a specific legal and financial context.

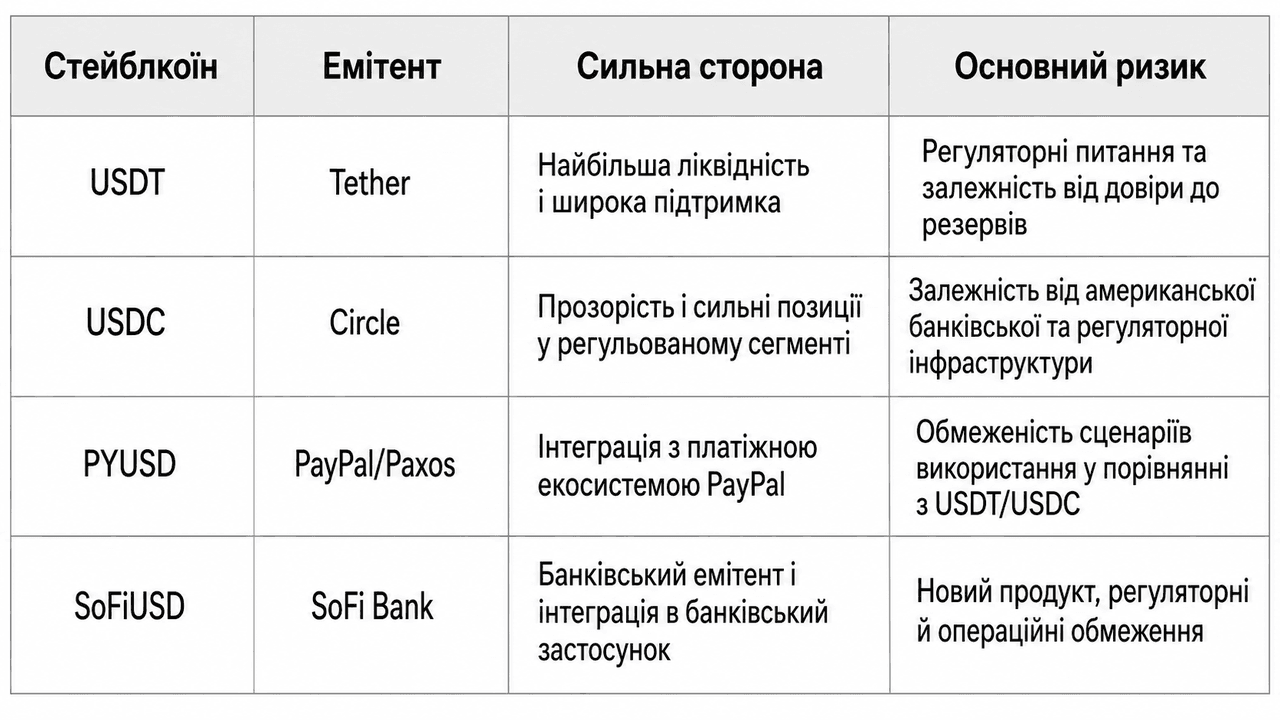

SoFiUSD vs. USDT, USDC, and PYUSD

SoFiUSD enters a competitive field where there are already strong players. USDT has the highest liquidity and is used on most exchanges. USDC bets on reserve transparency and regulatory clarity. PYUSD is integrated with the PayPal ecosystem.

The main difference of SoFiUSD is its banking nature. But trust in a bank does not eliminate the need to check terms of use, reserves, network availability, and the legal status of the token.

Can banks issue stablecoins

Yes, banks can issue stablecoins if their jurisdiction, regulatory bodies, and internal risk management model allow it. SoFiUSD has become an important example precisely because it is issued by an American national bank, not a classic crypto company.

But a bank stablecoin is not automatically a "safer cryptocurrency." Its safety depends on reserves, the owner's legal rights, the issuer's transparency, technical infrastructure, regulatory oversight, and redemption terms.

For banks, such a product can be part of a broader strategy: digital settlements, tokenized deposits, payment services, international transfers, and programmable finance.

The future of digital finance and Web3

SoFiUSD is interesting not just as an individual token. It shows how traditional finance is trying to integrate blockchain without completely abandoning the regulatory logic of the banking system.

In the future, we can expect more hybrid models: tokenized deposits, stablecoins from banks, digital bonds, smart contracts for corporate settlements, and payment networks that support multiple types of digital assets.

At the same time, Web3 will not automatically become safe just because banks are entering it. Increased institutional participation may improve transparency, but it may also increase centralization, access control, and dependence on large providers.

Tokenization of finance and the digital economy

Tokenization is the transfer of rights or the value of an asset into a digital token. In finance, this can apply to deposits, bonds, funds, stocks, real estate, or payment instruments.

SoFiUSD in this context is one of the elements of a larger process. It can be used as a unit of account for digital payments, but tokenized deposits or other banking products may appear alongside it.

For the user, the main question is simple: what exactly am I holding—a deposit, a stablecoin, a tokenized asset, or a claim against the issuer? The answer determines the risks, rights, taxes, and the ability to recover funds.

Risks and challenges of bank stablecoins

Bank stablecoins often seem safer than crypto-native assets, but they have their own set of risks.

Among the key risks of SoFiUSD:

- it is not a deposit and not an insured banking product;

- SoFiUSD is not covered by insurance from the Federal Deposit Insurance Corporation (FDIC) or the Securities Investor Protection Corporation (SIPC);

- SoFiUSD is not legal tender;

- blockchain transactions can be irreversible;

- access can be limited by jurisdiction, KYC, AML, and sanctions rules;

- technical glitches in the network or app can affect transfers;

- the new product has a shorter history of market use than USDT or USDC.

There is also a broader systemic risk. If banks massively issue their own stablecoins, the market could become more fragmented: one token for one banking ecosystem, another for a payment network, a third for corporate settlements. This increases the role of interoperability between networks and regulatory regimes.

Questions and answers

What is SoFiUSD?

SoFiUSD, or SOFID, is a payment stablecoin pegged to the US dollar, issued by SoFi Bank. It is intended for digital payments, blockchain settlements, and use within the SoFi infrastructure.

How does SoFiUSD differ from USDT and USDC?

The main difference is the banking issuer. USDT is issued by Tether, USDC by Circle, and SoFiUSD by SoFi Bank. This can be important for trust and compliance, but it does not eliminate technical, regulatory, and market risks.

Is SoFiUSD a bank deposit?

No. SoFiUSD is not a bank deposit, is not insured by the FDIC or SIPC, is not legal tender, and may lose value.

Can SoFiUSD be used in Ukraine?

Availability depends on SoFi's rules, the user's jurisdiction, and requirements. In Ukraine, the hryvnia remains the only legal tender, and the regulation of virtual assets is still being formed.

Will stablecoins replace banks?

Probably not. But they can change individual banking processes: international transfers, settlements, tokenized deposits, and payment infrastructure.

What is the future of bank stablecoins?

Their role may grow if banks, payment networks, and regulators find a balance between blockchain speed, reserve transparency, user protection, and financial control. But this development depends on rules in the US, EU, Ukraine, and other jurisdictions.

Conclusion

SoFiUSD is an important example of how the banking sector is entering the world of digital assets not through speculative tokens, but through payment infrastructure. Its launch in the SoFi app shows that stablecoins are becoming part of a broader financial system where blockchain is used for settlements, transfers, and potential asset tokenization.

The advantages of SoFiUSD are clear: a dollar peg, a banking issuer, support for public blockchains, and potential use in payment networks. But the risks are just as real: lack of deposit insurance, irreversibility of transactions, regulatory restrictions, and dependence on the issuer's rules.

For Ukrainian readers, the main conclusion is this: SoFiUSD should be viewed as a foreign digital asset, not as an alternative to the hryvnia or a risk-free banking product. It may be part of the future payment infrastructure, but any use of stablecoins requires an understanding of legal status, taxes, compliance, and technical risks.

For those who want to delve deeper into different types of stablecoins, the WEEX Cryptopedia has separate materials on stablecoins, crypto-risks, and the basic infrastructure of digital assets.

DISCLAIMER

WEEX and its affiliates provide digital currency exchange services, including derivatives and margin trading, only where such activity is legal and exclusively to appropriate users. All content is provided for reference only and does not constitute financial advice—seek advice from a financial advisor before trading. Cryptocurrency trading is high-risk and can result in the loss of your entire investment. By using WEEX services, you accept all associated risks and terms. Always invest only the amount you can afford to lose. Details are available in our Terms of Use and Risk Warning.

Customer Support:@weikecs

Business Cooperation:@weikecs

Quant Trading & MM:bd@weex.com

VIP Program:support@weex.com